What you need to know

The technology sector faces another challenge as its go-to specialized bank, Silicon Valley Bank, collapsed after a bank run.

The hard-hit tech sector first made news in late 2022 and early 2023 with mass layoffs. This collapse is another setback for the tech industry and is the biggest bank failure since Washington Mutual in 2008.

The U.S. government stepped in to protect customer deposits, and HSBC plans to purchase the U.K. portion of Silicon Valley Bank (SVB).

Here’s what happened to SVB and how it may affect tech companies and startups moving forward.

What is Silicon Valley Bank?

SVB was founded in 1983 and was the 16th largest U.S. bank before its collapse. They specialized in financing and banking for venture capital-backed startup companies — mostly technology companies. Venture capital firms did business there as well as several tech executives.

Based in Silicon Valley, SVB had assets totaling $209 billion at the end of 2022, according to the Federal Deposit Insurance Corporation (FDIC).

Why was SVB important to the tech sector?

SVB provided financing for about half of all U.S. venture-backed technology and healthcare companies. SVB was a preferred bank for the tech sector because they supported startup companies that not all banks would accept due to higher risks.

The pandemic in 2020 was a hot market for tech companies as consumers spent big money on digital services and electronics. Tech companies had a large influx of cash, and SVB’s services were needed during this time to hold their cash for business expenses, such as payroll. The bank invested much of these deposits as banks typically do.

Why did it collapse?

The collapse happened for multiple reasons, including a lack of diversification and a classic bank run, where many customers withdrew their deposits simultaneously due to fears of the bank’s solvency. Many of SVB’s depositors were startup companies. They deposited large amounts of cash from investors because tech was in high demand during the pandemic, said Jay Jung, founder and managing partner of Embarc Advisors.

Lack of diversification

Silicon Valley Bank invested a large amount of bank deposits in long-term U.S. treasuries and agency mortgage-backed securities. However, bonds and treasury values fall when interest rates increase.

When the Federal Reserve hiked interest rates in 2022 to combat inflation, SVB’s bond portfolio started to drop. SVB would have recovered its capital if they held those bonds until their maturity date.

Silicon Valley Bank used to lend out money in short durations. However, in 2021, they shifted to long-term securities such as treasuries for more yield, and they did not protect their liabilities with short-term investments for quick liquidations. They were insolvent for months because they could not liquidate their assets without a large loss.

When economic factors hit the tech sector, many bank customers withdrew money as venture capital started drying up. SVB didn’t have the cash on hand to liquidate these deposits because they were tied up in long-term investments. They started selling their bonds at a significant loss, which caused distress to customers and investors.

Within 48 hours after disclosing the sale of assets, the bank collapsed.

Bank run

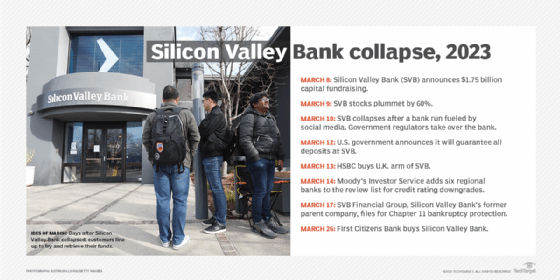

When SVB announced their $1.75 billion capital raising on March 8, people became alarmed the bank was short on capital. Word spread quickly on social media accounts such as Twitter and WhatsApp inducing panic that the bank didn’t have enough funds. Customers started to withdraw money in waves. SVB’s stock plummeted by 60% on March 9 after its capital raising announcement. Some people are saying the bank run was Twitter-fueled.

California regulators shut the bank down on March 10 and placed SVB under the FDIC.

Unlike personal banking, SVB’s clients had much larger accounts. It didn’t take long for money to diminish during the bank run, with the escalating pace of withdrawals causing a snowball effect. Most customers had deposits more than the $250,000 FDIC limit.

Many startups left money in their SVB primary account instead of using other accounts — such as a money market — to pay expenditures. This means most of their working capital was mainly in their SVB account, and they needed access to their deposits for payroll and bills.

Who is affected by the collapse?

SVB stockholders and investors took a big hit because, unlike customers, they were not backed by FDIC on their investment.

Other issues include a lack of money from deposits for immediate expenses such as payroll. Large tech companies with significant cash in SVB include Etsy, Roblox, Rocket Labs and Roku.

The FDIC insures most banks. However, the accounts were insured up to only $250,000. With company accounts, this is not much, as they may spend millions in a month.

First Citizens Bank purchases Silicon Valley Bank

On March 26, 2023, FDIC announced First Citizens Bank will purchase Silicon Valley Bank and assume the majority of its deposits and loans. As of March 10, Silicon Valley Bank reported nearly $167 billion in total assets and $199 billion in deposits. First Citizens Bank will purchase about $72 billion in assets at a discounted rate of $16.5 billion. FDIC will remain in control of nearly $90 billion in assets and securities in its receivership.

All 17 of Silicon Valley Bank’s branches will operate under Silicon Valley Bank, a division of First Citizens Bank.

The FDIC also estimated that the SVB failure cost nearly $20 billion.

More bank issues

In addition to Silicon Valley Bank, other banks were facing solvency issues such as Signature Bank and Credit Suisse. UBS agreed to buyout Credit Suisse for $3 billion Swiss francs (or $3.25 billion) in a government-brokered deal on March 19.

New York Community Bank agreed to buy a large portion of Signature Bank in a $2.7 billion deal on March 19, according to the FDIC. The branches of Signature Bank will be called Flagstar Bank, which is one of New York Community Bank’s subsidiaries.

On March 14, Moody’s Investor Service put six regional banks on review for credit rating downgrades, including Comerica Bank, First Republic Bank, Intrust Financial, UMB Financial, Western Alliance Bancorporation and Zions Corp. The reasons for these ratings include high unrealized losses and large amounts of deposits not covered by FDIC. These are issues that also impacted SVB.

What is the Federal Reserve doing?

The government is not bailing out SVB. It will stay collapsed, and the remaining assets will go to creditors. A buyer can bring it back to life if another bank purchases it.

On March 12 the government guaranteed to cover all deposits at SVB. However this guarantee does not include shareholders or unsecured creditors. Silicon Valley Bank is closed, so the FDIC formed the Deposit Insurance National Bank of Santa Clara to consolidate insured and uninsured deposited into one institution.

All deposits of SVB were transferred to the National Bank of Santa Clara, and insured depositors had access to their funds on March 13. The FDIC will pay uninsured depositors an advanced dividend. They will receive a certificate with the remaining amount of their uninsured funds to receive remaining funds when the FDIC sells SVB’s assets.

The turmoil of bank stocks may make the Federal Reserve more cautious when raising rates. The larger banks are well-hedged and diversified, but regional banks may feel the tightening of the market if they are tied to industries that tend to be more cash strapped like tech startups.

The FDIC usually will sell a failed bank’s assets to others. Those proceeds will repay uninsured depositors.

Silicon Valley Bank’s former parent company, SVB Financial Group, filed for Chapter 11 bankruptcy protection on March 17. This filing came after Silicon Valley Bank shareholders targeted SVB Financial Group in a civil lawsuit. Administrators will sell off assets to pay off creditor claims.

Silicon Valley Bank is not a part of this bankruptcy filing because they are under the control of the FDIC.

How could this collapse affect small businesses and the financial sector in the future?

Immediate panic may subside with the U.S. government’s guarantee of bank customer deposits. Stocks and financial futures increased after the guarantee by 1% to 2%. Before the guarantee, SVB customers were worried about paying employees, which would have upset the economy even more.

The larger questions involve the rising interest rates and if other banks are too invested in falling bond prices. The Federal Reserve created a new program named the Bank Term Funding Program, which provides loans to banks and credit unions for money tied into U.S. Treasury and mortgage-backed securities to meet the demands of customers. This program prevents banks selling long-term government securities for a loss during stressful times.

The biggest concern right now is the technology sector, which has been hit with recessionary conditions, forcing larger tech companies to cut staff. Now one of their largest supporters has collapsed. Startups may face funding issues as management teams at other banks are scared to take the risk of the investment, Jung said.

In the broader scope, SVB’s collapse shows that financial management is necessary when times are good and bad. Jung said during a recessionary environment, companies need to take extra precautions with rising interest rates, supply chain issues and difficulties in raising capital.

Is money safe in the bank moving forward?

According to experts, money is safe in the banks as long as consumers take some precautions. People should plan accordingly and stay within the FDIC insurance limits and spread out accounts as much as possible, said Frank Arellano, founder and CEO of Revolv3, a subscription billing platform. He also said some banks are offering additional insurance above FDIC, and businesses and consumers should make sure all their deposits are insured.

Having multiple accounts is another way to diversify funds. For example, customers should have at least two bank accounts and one investment account to move money around, Jung said.

Startup funding may be a little harder, and scrutiny is different when evaluating risks. If startups can show they are managing finances and have a strong balance sheet, there are venture capital investors that are still available, Arellano said.

“I think we will get over this hump, and this banking stuff will be yesterday’s news,” Jung said. “Business owners can focus on running their businesses.”

One year after the SVB collapse

One year later, the SVB collapse still stands out as one of the biggest bank failures in American history. According to a new report by Bloomberg, SVB’s bankruptcy resulted in the biggest fine since the financial crisis of 2008. The $285 million fee was in penalties to retire emergency financing secured through the Federal Home Loan Bank (FHLB) system, which supports mortgage lending. SVB applied for billions of dollars in funding from FHLB to survive the large amounts of deposit withdrawals.

FHLB had the option to recall its funding after the collapse, but it declined to do so. The bridge bank that took control of SVB’s assets decided to repay advances early and now faces these large penalties outlined in the contract.

There are still questions since the banking industry is changing and there could be further crises, which would make the financial system less resilient.

After the collapse, business owners have started to look at business banking a little differently, including using more than one financial institution to spread out cash for protection and diversification. There is also a large demand for venture debt, as this was SVB’s specialty and finding the right funding may be more difficult.

link