")

toeytoey2530/iStock via Getty Images

Molecular Partners AG (NASDAQ:MOLN) (OTCPK:MLLCF) is a clinical-stage biotechnology pioneering the development of designed ankyrin repeat proteins [DARPins] to treat oncology and virology illnesses. DARPins offer several advantages over traditional antibodies, such as higher specificity, stability, and versatility, making them highly effective in treating complex diseases like cancer. The Switch-DARPin platform has shown promising preclinical results, demonstrating conditional and reversible immune activation in vivo. This advance is particularly beneficial for vulnerable populations like older patients or those with comorbid conditions, providing targeted and customizable therapy alternatives with reduced toxicity. Despite the inherent biotech risks, I lean bullish on MOLN due to its highly differentiated IP and sufficient resources for the foreseeable future.

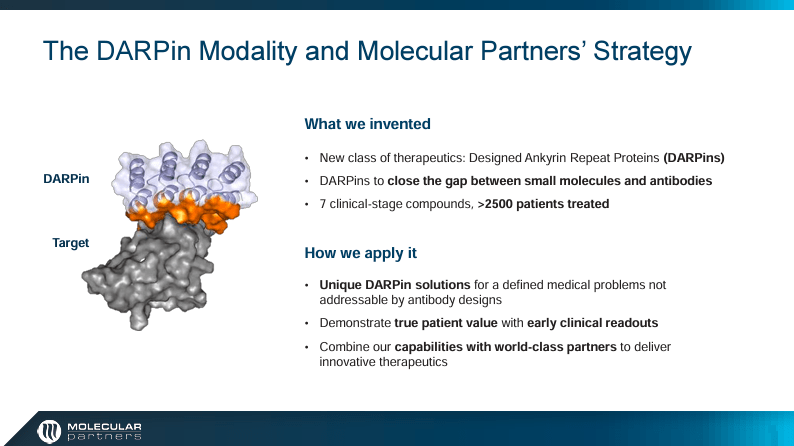

DARPin: Business Overview

Molecular Partners is a clinical-stage biotechnology company based in Schlieren, Switzerland. The company was founded in 2004 and went public on NASDAQ on June 16, 2021. Today, MOLN develops ankyrin repeat protein [DARPin] treatments for oncology and viral diseases. The company’s DARPin modality and molecular strategy address specific solutions for medical conditions that standard antibody designs cannot solve. Concretely, in oncology, MOLN directly targets malignant cells or modulates the immune response within the tumor. As for virology, it refers to killing viruses or regulating immune reactions to fight viral infections.

Source: Corporate Presentation. June 2024.

MOLN uses its proprietary designer proteins because they have six key advantages over traditional antibodies in various diseases. First, 1) DARPins are engineered to reach higher specificity and affinity for targets with greater precision than conventional antibodies. Also, 2) DARPins use multiple binding domains, which can enhance their adaptability and binding power compared to conventional antibodies’ typical single or dual binding sites. 3) DARPins maintain more structural stability under diverse conditions and are less predisposed to denaturation than antibodies. Additionally, 4) DARPins have a modular nature that allows them to target different objectives. This characteristic is useful in conditions like cancer, where addressing multiple pathways improves medicinal efficacy.

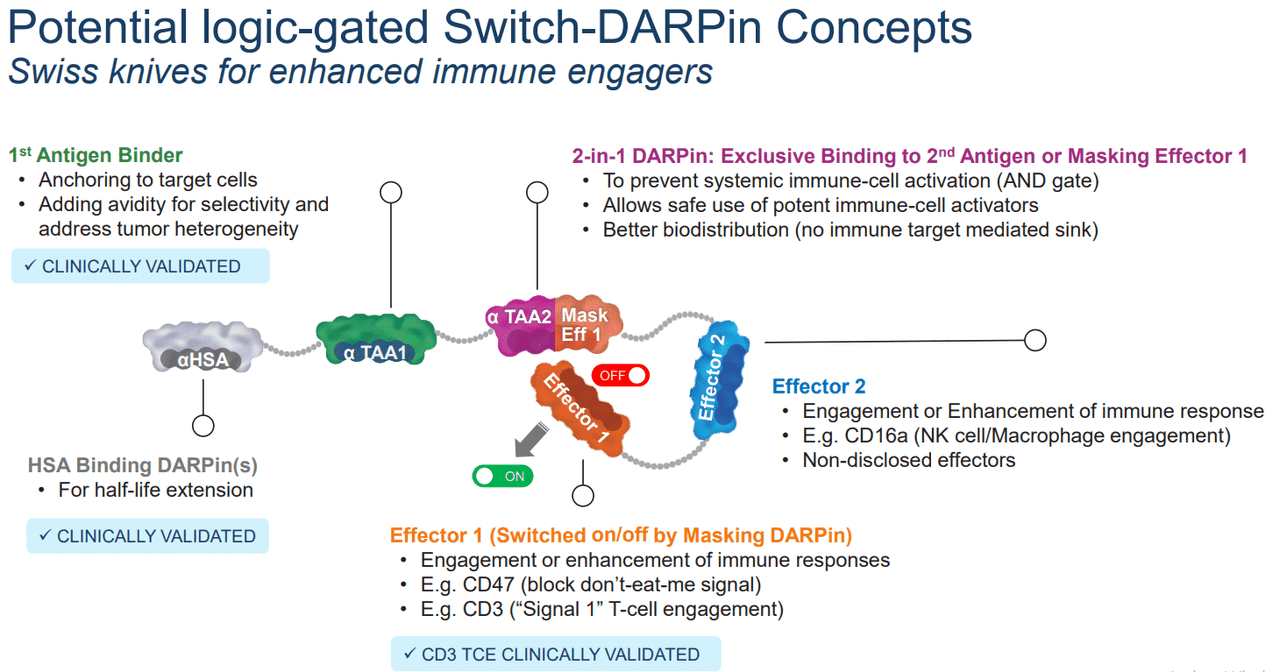

Furthermore, MOLN’s Switch-DARPin platform creates proteins that can alternate between targets depending on specific markers’ conditional activation or inhibition. This is key because 5) DARPins are engineered to reduce adverse immune responses, achieved through particular design strategies, improving the original function of regular human proteins. Lastly, 6) DARPins are smaller than antibodies, facilitating penetration into solid tumors.

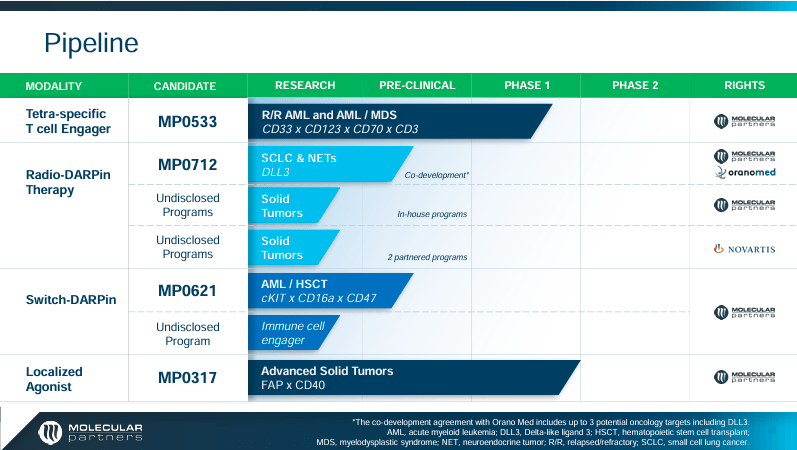

DARPin Platform: Product Pipeline

DARPins can be combined with radioactive isotopes to deliver radiation to cancer cells, reducing damage to healthy cells. These features illustrate why MOLN’s DARPins are theoretically an improvement over the current standard of care in oncology and virology. This science, including in-house programs, lies at the core of the company’s pipeline.

Source: Corporate Presentation. June 2024.

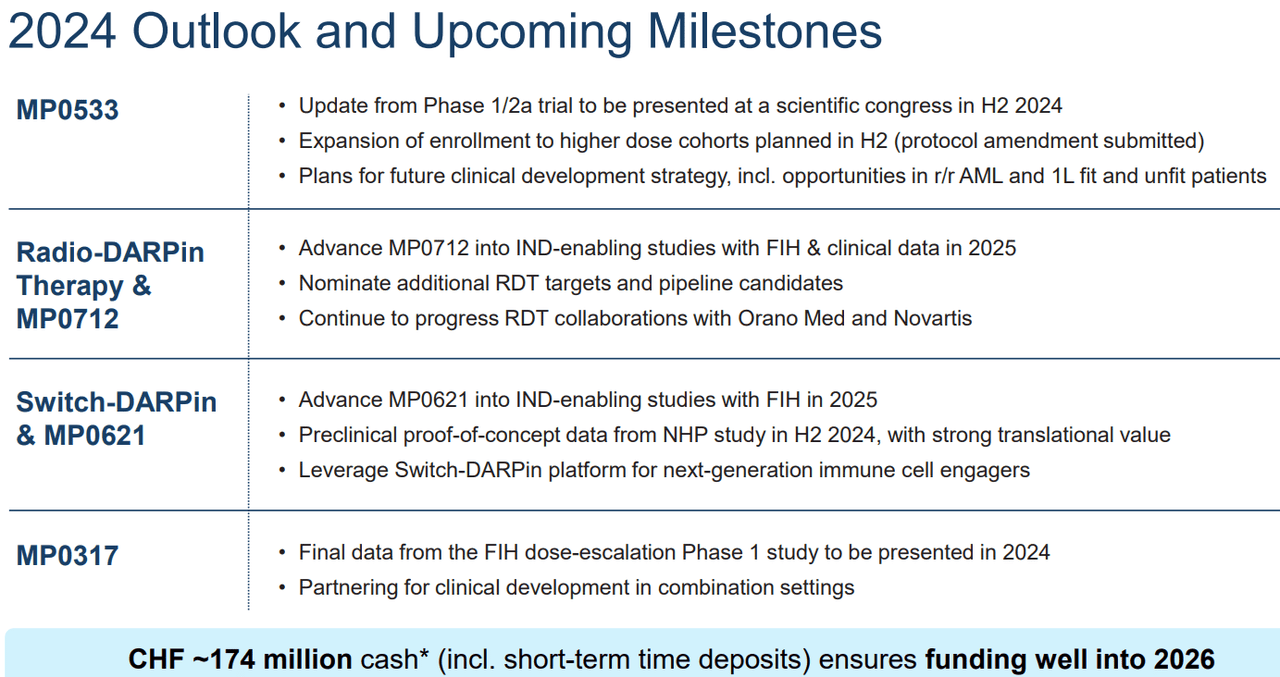

The company has a 1) tetra-specific T-cell engager called MP0533 in Phase 1 for relapsed/refractory acute myeloid leukemia [AML] and myelodysplastic syndromes [MDS]. MOLN also has 2) a pre-clinical Switch-DARPin called MP0621 for AML and hematopoietic stem cell transplant [HSCT]. The company is also working on a 3) tumor-localized CD40 agonist called MP0317 in Phase 1 for advanced solid tumors.

On the other hand, MOLN’s partnerships include MP0712, a Radio-DARPin therapy for treating small cell lung cancer [SCLC], and neuroendocrine tumors [NETs]. MP0712 is a preclinical stage project in collaboration with Orano Med. It’s also worth highlighting that MOLN has several preclinical undisclosed programs in Radio-DARPin therapy. Some are in-house programs, but two are part of its partnership with Novartis.

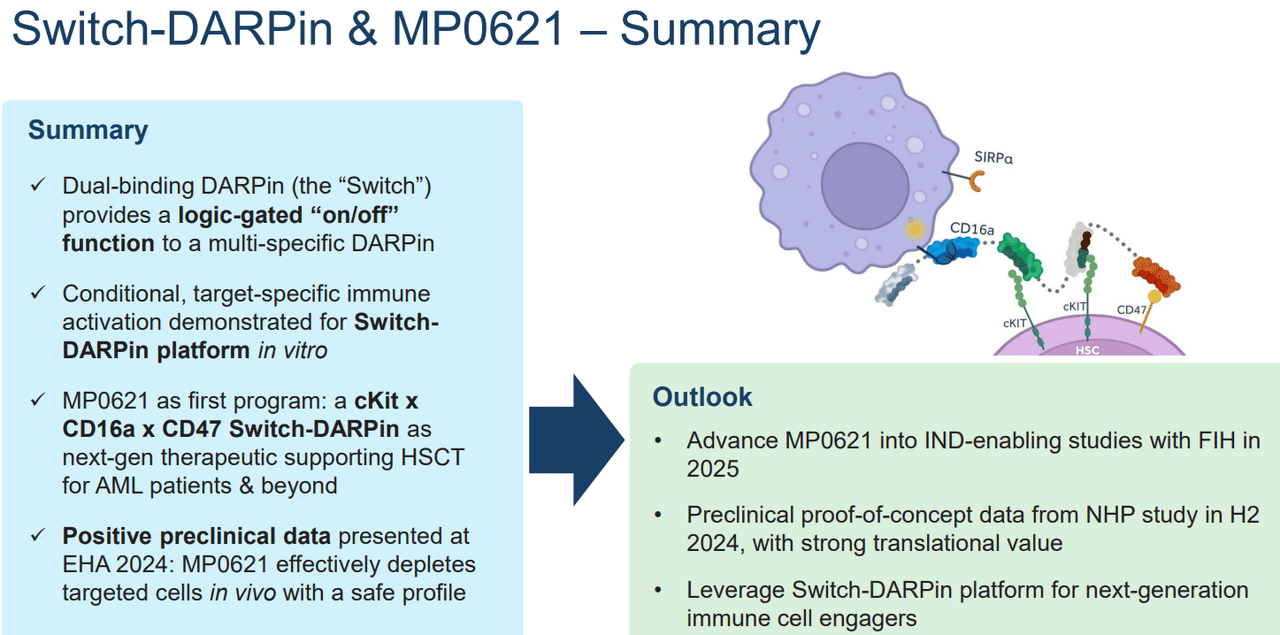

Showcasing Switch-DARPin: MP0621

In June 2024, MOLN reported promising preclinical data for its Switch-DARPin drug candidate. However, the results are more of a proof-of-concept regarding its platform using in vivo studies. This preclinical data showcases MOLN’s Switch-DARPin platform effectiveness in living organisms with conditional immune activation mechanisms using precise biomarkers. If necessary, MOLN’s platform can reverse biomarker activation and reduce adverse effects, deactivating after therapeutic results are accomplished. This reversibility feature is impressive because it theoretically improves the treatment’s safety profile, especially if used in oncology. If there are unintended immune activations during treatment, MOLN could simply deactivate the treatment and stop its adverse effects.

Source: Corporate Presentation. June 2024.

Note that MP0621 is the company’s first drug candidate generated for its Switch-DARPin platform. MP0621 is indicated for AML and other malignant and non-malignant diseases. Typically, HSCT can potentially cure AML and other hematologic conditions by replacing diseased bone marrow with healthy stem cells. However, before undergoing HSCT, patients must receive high-dose chemotherapy or radiation therapy to destroy the diseased bone marrow. This pre-transplant conditioning is necessary to make space for new stem cells, but typically provokes high toxicity in patients. This high toxicity can be deadly for older populations, limiting its use due to comorbid conditions. Moreover, if these vulnerable patients undergo pre-HSCT conditioning with reduced intensity, the odds of relapse increase because cancerous cells are likely to remain in the bone marrow.

Source: Corporate Presentation. June 2024.

Therefore, MOLN’s Switch-DARPin is potentially advantageous in these cases. MP0621 delivers targeted immune system activation in the presence of disease markers, reducing off-target reactions. This is beneficial for those demographics and lowers their relapse risk without increased toxicity. It introduces the concept of using customizable therapies for different patient populations. These impressive IND-enabling results justify MOLN’s Phase 1 trials for AML, which management anticipates will begin by 2025. More importantly, the company’s Switch-DARPin platform opens up exciting treatment alternatives for vulnerable populations due to the adverse effects of aggressive therapies.

Differentiated IP: Valuation Analysis

From a valuation perspective, MOLN trades at a $203.7 million market cap, making it a microcap biotech. It’s also technically a foreign company based in Switzerland, but its clinical trials comply with FDA regulations, so it also targets US markets. Moreover, it reports its financial statements in Swiss CHF, but we can convert those figures to USD at the current exchange rate (1.17 CHF/USD as of August 2024). Thus, MOLN’s balance sheet holds $80.0 million in cash and equivalents and $123.8 million in short-term deposits. Its available short-term liquidity is $203.8 million against no financial debt other than operating lease liabilities. Its total liabilities amount to $20.0 million, with a book value of $197.2 million. This indicates that MOLN has a 1.0 P/B ratio, which is relatively cheap. For comparison, its sector median P/B is 2.3, suggesting MOLN might be somewhat undervalued.

Source: Corporate Presentation. June 2024.

Furthermore, I estimate its latest quarterly cash burn was $20.1 million by adding its CFOs and Net CAPEX. This indicates a cash runway of about 10.1 quarters, which should be enough until late 2025. However, management expects MOLN to have enough resources until 2026, which might be slightly optimistic at the current cash burn rate. I imagine management will moderate its cash burn in the following quarters to meet that target. However, this will be challenging as it plans on executing concurrently multiple clinical trials. So, the likelihood of capital raises in the next few years seems high, considering that it only has preclinical and Phase 1 research projects. Therefore, obtaining any potential FDA approvals will still take several years.

Source: Corporate Presentation. June 2024.

It’s worth highlighting that MOLN’s unique Switch-DARPin technology is likely its main value driver at this juncture. This is undoubtedly its most unique asset, in my view, especially because of its “on/off” clinically validated feature through masking DARPin. This is still a highly speculative asset, as there are no FDA-approved drugs with this technology yet. However, I think it’s a differentiator from an investment perspective.

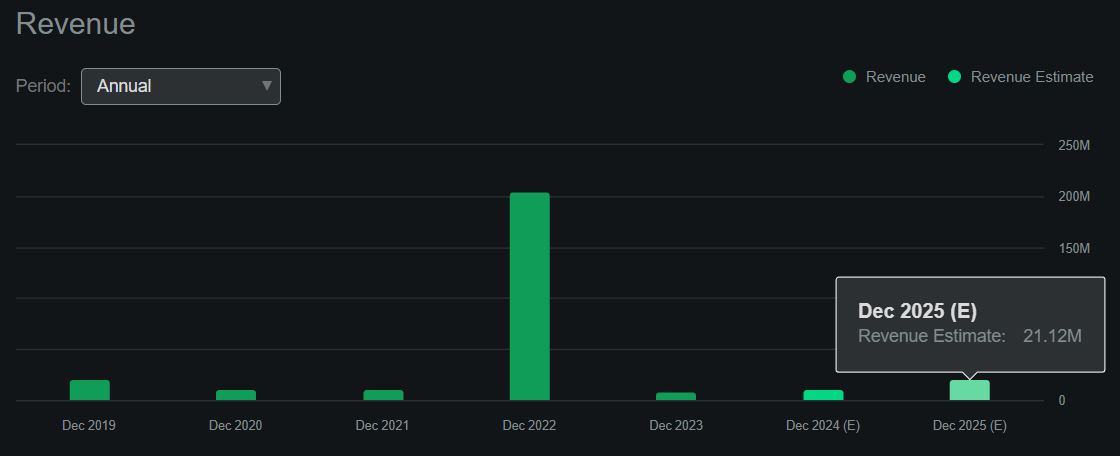

Additionally, MOLN generates some collaboration research revenues, further corroborating its IP’s attractiveness. According to Seeking Alpha’s dashboard on MOLN, the company should generate about $21.1 million in revenues (likely from collaborations) by 2025. This implies that MOLN has a somewhat high P/S multiple of 9.7. For context, its sector median forward P/S ratio is 3.5, so in this sense, MOLN appears relatively expensive.

Source: Seeking Alpha.

Nonetheless, I think MOLN’s valuation seems compelling as it trades below its available short-term liquidity of $203.8 million and has highly differentiated IP. Since these figures are originally in CHF, it also exposes investors to currency advantages if the USD declines due to Fed rate cuts in September 2024. On the other hand, I also recognize that MOLN’s IP is still highly speculative and in the early stages. Thus, I think it makes sense to lean slightly bullish on MOLN, which is why I rate it a speculative “buy” for investors looking into unique oncology and virology biotechs.

Investment Caveats: Risk Analysis

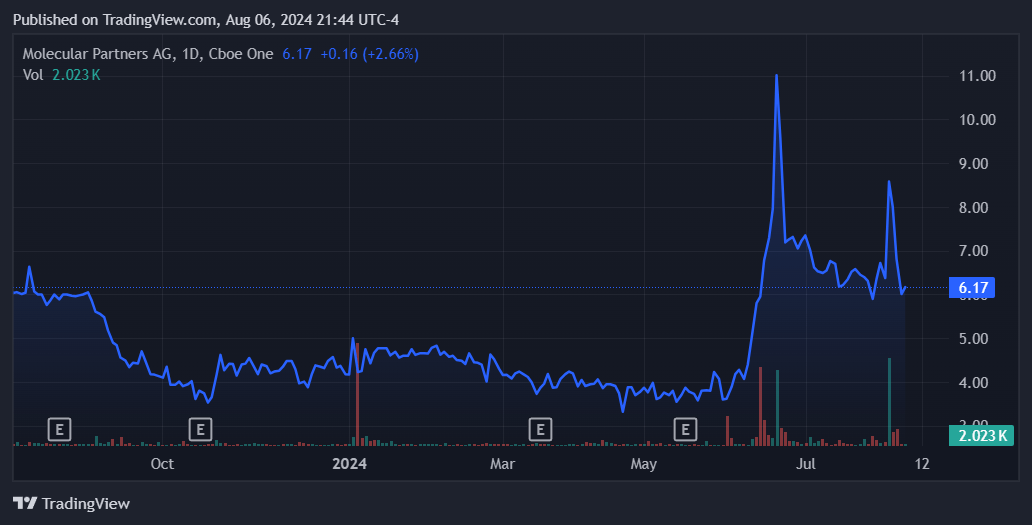

Naturally, investors must remember that this speculative “buy” thesis hinges on MOLN’s unique Switch-DARPin technology and its seemingly compelling valuation. However, the reality is that MOLN’s IP has not yet been proven. If further clinical trials on its drug candidates show low effectiveness or a concerning safety profile, then all of MOLN’s IP could be threatened. This would undoubtedly lead to shareholder losses, especially because MOLN’s main tangible asset is its cash. Since its cash burn should last at most until 2026, the company will gradually erode that tangible value over the next few years. If there are no remarkably positive results at the end of its trials, it could leave investors in a precarious position, potentially facing considerable dilution risks.

Source: TradingView.

Even in the best-case scenario where MOLN’s Switch-DARPin technology yields results, it’s still probable that the company will require additional funding to advance its research to potential FDA approval and commercialization. Moreover, this is inherently a long-term bet, as the research will still take several years to progress toward a possible FDA approval. Still, I think MOLN’s technology and current valuation justify a bullish outlook. As long as investors size their positions carefully, MOLN could prove a viable speculative investment.

Speculative “Buy”: Conclusion

Overall, MOLN emerges as a highly speculative investment, but its uniquely differentiated approach to oncology and virology justifies this view. MOLN’s Switch-DARPin technology could pave the way to a new treatment paradigm where therapies can be activated and deactivated at will, depending on the patient’s responses. This approach could also have a superior safety profile compared to current alternatives and might even be more effective as well due to its highly targeted nature. I also estimate the company has enough resources to operate for the next few years, although I concede there are some long-term dilution risks. Thus, I deem MOLN a speculative “Buy” for investors who understand the embedded biotech risks and can position size accordingly.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

link